Running a small business in South Africa is exciting — but tax mistakes can quietly cost you money, credibility, and even funding opportunities.

Many business owners don’t intentionally avoid tax — they simply don’t understand the system.

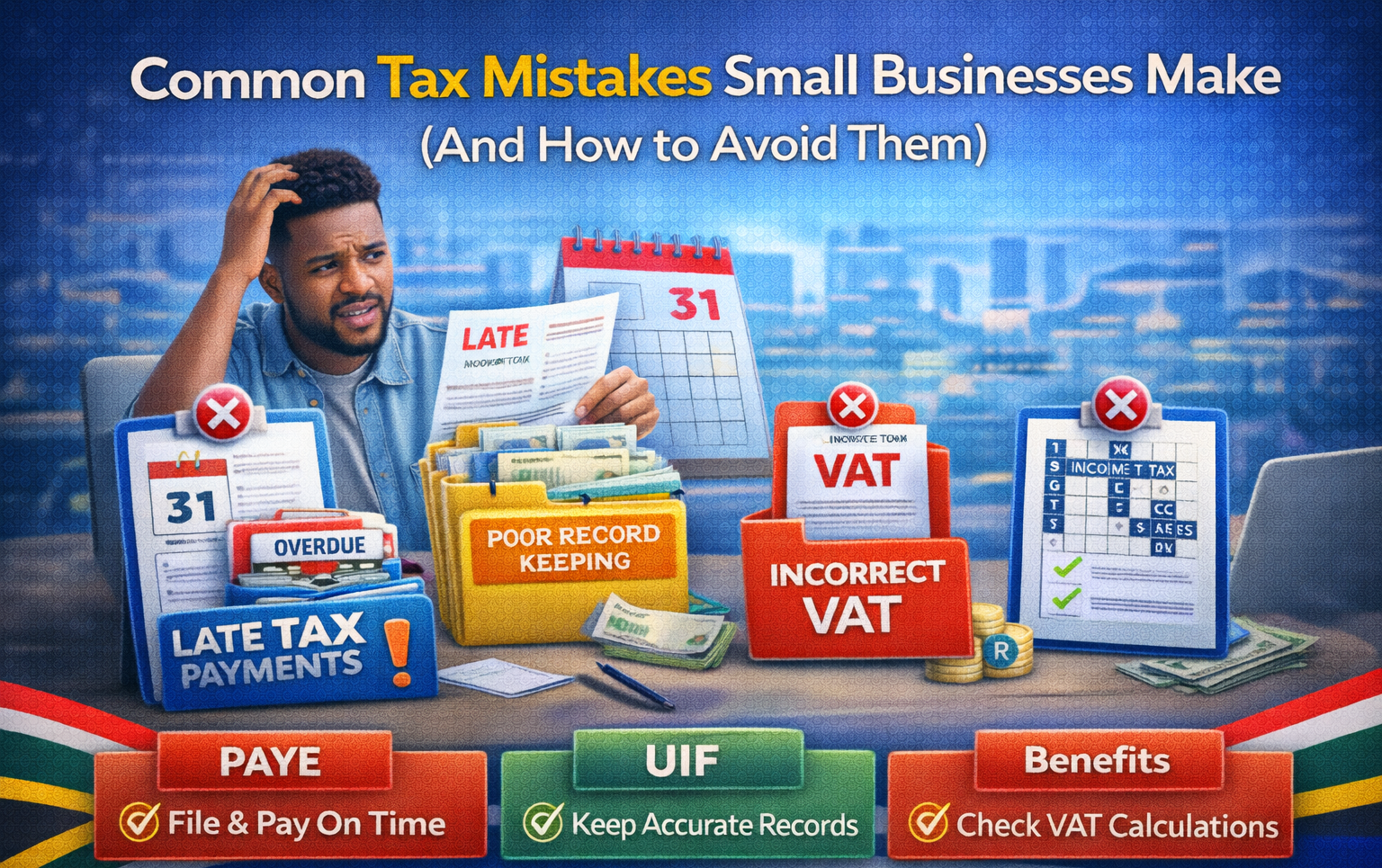

Let’s look at the most common tax mistakes small businesses make and how to avoid them.

Not Registering for Tax at All

Some entrepreneurs assume:

-

“I’m too small.”

-

“I just started.”

-

“I’m not making profit yet.”

But once you register a company with

Companies and Intellectual Property Commission (CIPC)

you are automatically required to comply with tax laws.

And if you operate as a sole proprietor, you are still required to register for income tax if you earn above the threshold.

Ignoring tax registration can lead to penalties and blocked funding applications.

Missing Tax Return Deadlines

One of the most common mistakes is:

❌ Not submitting returns on time

❌ Forgetting to file “nil” returns

❌ Ignoring SARS reminders

The

South African Revenue Service (SARS)

charges penalties for late submissions — even if you owe no money.

Important: Submitting returns is mandatory, even if your business made no income.

Mixing Personal and Business Finances

This causes serious confusion during tax season.

Common issues:

-

Using one bank account for everything

-

Paying personal expenses from business funds

-

No clear record of income

This makes it difficult to:

-

Calculate profit correctly

-

Claim deductions

-

Prove compliance

Always separate business and personal accounts.

Registering for VAT Too Late (or Too Early)

Many businesses:

-

Forget that VAT registration becomes mandatory at R1 million turnover

-

Register too late and face penalties

-

Register too early without understanding cash flow impact

VAT requires strict record-keeping and regular submissions.

If unsure, get professional advice before registering voluntarily.

Not Keeping Proper Records

SARS may request:

-

Invoices

-

Receipts

-

Bank statements

-

Payroll records

If you cannot provide supporting documents, deductions may be denied.

Keep records for at least 5 years.

Use:

-

Accounting software

-

Organized digital folders

-

Monthly bookkeeping

Not Setting Aside Money for Tax

A very common mistake:

Spending all business income without reserving money for tax.

Remember:

-

VAT collected is not your money

-

PAYE deducted belongs to SARS

-

Income tax is calculated on profit

Open a separate “tax savings” account and transfer a portion monthly.

Ignoring PAYE, UIF & SDL Requirements

If you employ staff, you must register for:

-

PAYE

-

UIF

-

SDL (if payroll exceeds threshold)

Failure to register payroll taxes can result in audits and fines.

Many small businesses think they can delay this — but SARS can trace payments through banking records.

Not Applying for a Tax Clearance Certificate

Without tax compliance, you cannot:

-

Apply for government tenders

-

Access funding

-

Register on supplier databases

Maintaining good standing ensures your business opportunities remain open.

Underreporting Income

Some business owners:

-

Don’t declare cash sales

-

Omit side income

-

Guess revenue instead of calculating

This is risky and can trigger audits.

SARS uses data-matching systems to verify income from banks and third parties.

Transparency protects your business long-term.

Trying to Handle Everything Without Understanding Tax

Tax laws can be complex.

Common problems:

-

Misunderstanding allowable deductions

-

Incorrect VAT calculations

-

Filing wrong tax types

Getting guidance early can prevent years of compliance issues.

How to Avoid These Mistakes

✔ Register correctly

✔ Submit returns on time

✔ Separate business finances

✔ Keep accurate records

✔ Set aside tax money monthly

✔ Stay informed

Tax compliance is not just about avoiding penalties — it builds credibility.

Final Thoughts

Most tax problems don’t happen because businesses are dishonest — they happen because business owners are overwhelmed.

The good news?

Tax compliance becomes simple when you:

-

Understand your obligations

-

Stay organized

-

Act early

Avoiding these common mistakes protects your business, your funding eligibility, and your peace of mind.

Career Store